Map Shows Where Americans Are Falling Behind on Debt Payments

Summary

A new analysis finds that Americans owe much more debt now than 20 years ago, with average debt nearly doubling from about $33,000 in 2003 to over $63,000 in 2025. The study shows some states have higher debt burdens and are more likely to fall behind on payments, especially with mortgages, credit cards, and student loans.Key Facts

- Average individual debt in the U.S. rose from $32,840 in 2003 to $63,200 in 2025.

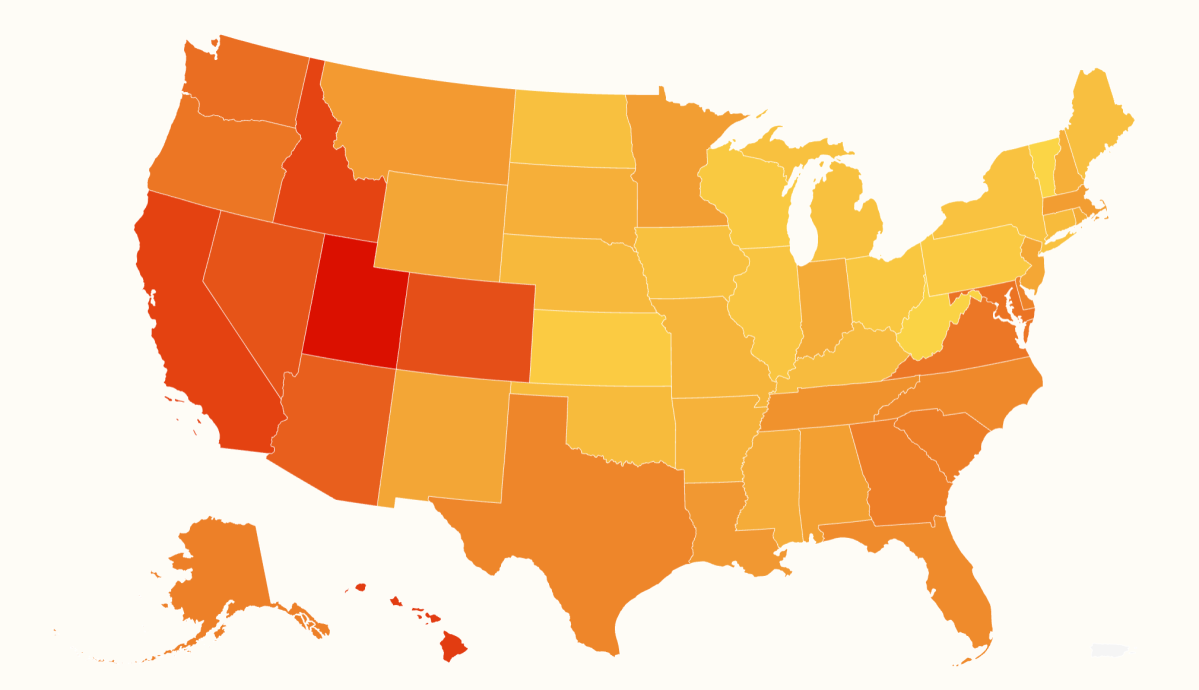

- The average American income is estimated at $45,256, but debt is 139.6% of income on average.

- Utah has the highest debt-to-income ratio at 199.4%, meaning residents owe nearly twice what they earn yearly.

- Despite high debt, Utah’s residents have lower rates of falling behind on payments.

- Louisiana has the highest rate of missed mortgage payments and a debt-to-income ratio of 136.1%.

- Nevada ranks third due to a high credit card delinquency rate of 16.3% and a debt-to-income ratio of 167.5%.

- Mississippi has the highest student loan delinquency rate at 13.4%, despite relatively low overall debt.

- Rising debt and low income mean unexpected costs like car repairs or doctor visits can cause big financial problems.

Read the Full Article

This is a fact-based summary from The Actual News. Click below to read the complete story directly from the original source.